All Categories

Featured

Table of Contents

Just pick any type of type of level-premium, long-term life insurance policy from Bankers Life, and we'll convert your policy without calling for evidence of insurability. Policies are convertible to age 70 or for five years, whichever comes later - compare decreasing term life insurance. Bankers Life supplies a conversion credit history(term conversion allowance )to insurance holders up to age 60 and through the 61st month that the ReliaTerm policy has been in force

:max_bytes(150000):strip_icc()/Investopedia-terms-termlife-6451fde927474d4f8a81a5681efd393f.jpg)

At Bankers Life, that implies taking a personalized method to help protect the individuals and family members we serve - term life insurance questions. Our goal is to supply exceptional solution to every insurance holder and make your life less complicated when it comes to your cases.

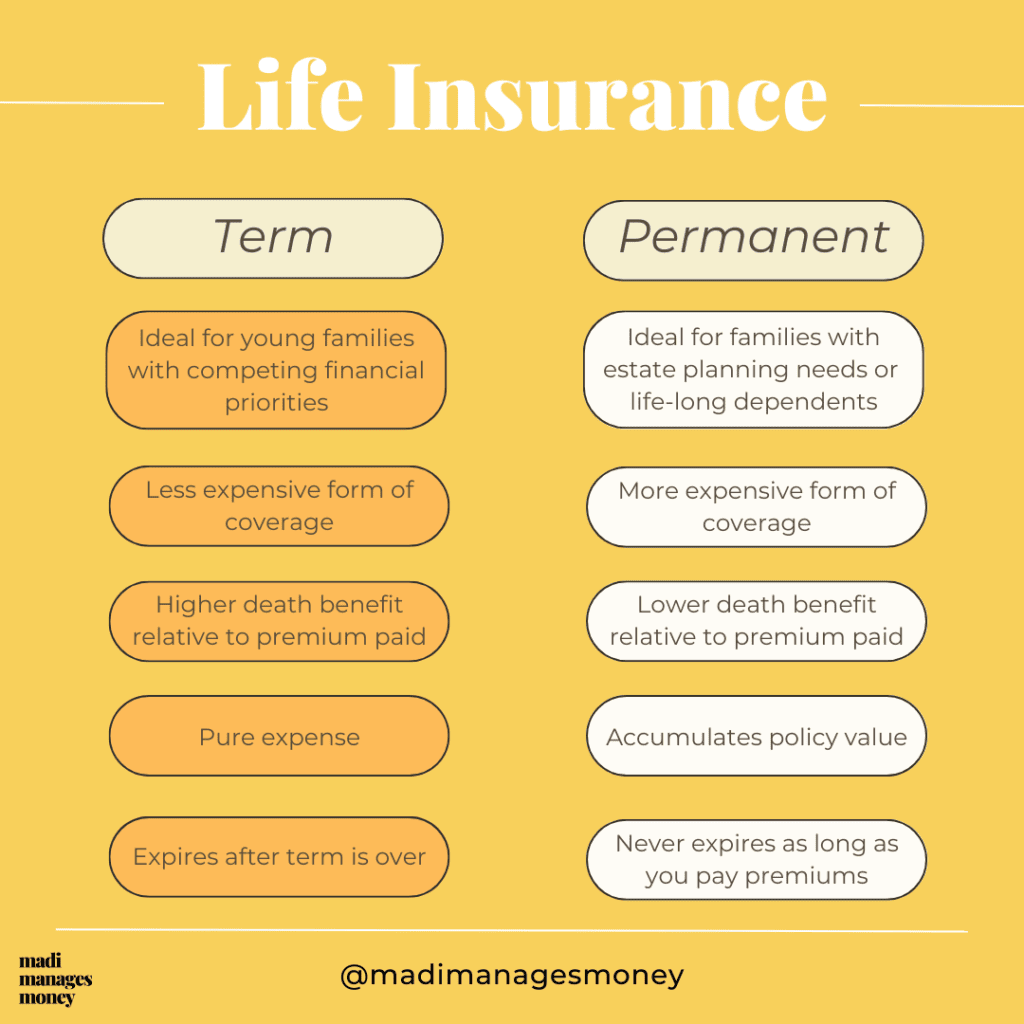

In 2022, Bankers Life paid life insurance coverage declares to over 658,000 insurance policy holders, completing$266 million. Bankers Life is certified by the Better Service Bureau with an A+ ranking since March 2023, in enhancement to getting an A( Superb)ranking by A.M. For the most component, there are two sorts of life insurance coverage plans-either term or long-term strategies or some mix of both. Life insurance firms offer numerous forms of term plans and conventional life policies along with "interest sensitive"products which have actually become extra prevalent because the 1980's. Term insurance policy supplies defense for a specific time period. This duration might be as brief as one year or give insurance coverage for a particular variety of years such as 5, 10, twenty years or to a specified age such as 80 or in some instances as much as the earliest age in the life insurance coverage death tables. Currently term insurance prices are really affordable and among the cheapest traditionally knowledgeable. It should be kept in mind that it is an extensively held belief that term insurance policy is the least expensive pure life insurance coverage readily available. One needs to evaluate the plan terms carefully to choose which term life alternatives are suitable to satisfy your particular scenarios. With each brand-new term the premium is raised. The right to renew the plan without proof of insurability is a crucial advantage to you (second to die term life insurance). Otherwise, the risk you take is that your wellness may weaken and you may be unable to get a policy at the same prices and even in any way, leaving you and your recipients without insurance coverage. You should exercise this choice throughout the conversion duration. The size of the conversion period will certainly differ depending upon the sort of term plan bought. If you convert within the proposed period, you are not called for to provide any info regarding your health. The costs price you

pay on conversion is typically based upon your"present attained age ", which is your age on the conversion date. Under a degree term plan the face amount of the policy remains the exact same for the entire duration. With lowering term the face amount minimizes over the period. The costs stays the very same yearly. Commonly such policies are offered as home mortgage defense with the quantity of.

:max_bytes(150000):strip_icc()/dotdash-term-life-vs-whole-life-5075430-Final-60fb4e8f7bae43e0a65a3fac2431479c.jpg)

insurance policy reducing as the balance of the mortgage reduces. Commonly, insurance companies have actually not deserved to change costs after the policy is marketed. Considering that such policies may continue for years, insurance providers need to use conservative death, interest and expenditure rate quotes in the costs estimation. Flexible costs insurance coverage, however, permits insurers to offer insurance policy at reduced" current "costs based upon less traditional assumptions with the right to alter these costs in the future. Under some policies, costs are required to be spent for a set variety of years. Under other policies, premiums are paid throughout the insurance policy holder's lifetime. The insurance provider spends the excess costs dollars This kind of policy, which is sometimes called cash money worth life insurance policy, creates a financial savings component. Money worths are essential to a long-term life insurance policy plan. Occasionally, there is no relationship between the size of the money worth and the premiums paid. It is the cash money value of the policy that can be accessed while the insurance holder lives. The Commissioners 1980 Standard Ordinary Mortality Table(CSO )is the current table used in computing minimum nonforfeiture worths and policy books for regular lifeinsurance coverage plans. Several long-term plans will certainly have provisions, which define these tax obligation demands. There are 2 basic categories of long-term insurance policy, typical and interest-sensitive, each with a variety of variations. In enhancement, each category is typically offered in either fixed-dollar or variable form. Traditional entire life plans are based upon long-lasting price quotes ofcost, interest and death. If these price quotes transform in later years, the firm will change the premium accordingly yet never over the maximum assured premium mentioned in the plan. An economatic whole life plan attends to a standard amount of participating whole life insurance policy with an additional extra protection given via the usage of dividends. Due to the fact that the premiums are paid over a much shorter span of time, the costs payments will certainly be higher than under the entire life plan. Solitary premium whole life is minimal settlement life where one large exceptional repayment is made. The policy is fully compensated and no additional costs are called for. Considering that a considerable payment is included, it should be considered as an investment-oriented product. Rate of interest in single costs life insurance is primarily as a result of the tax-deferred therapy of the accumulation of its cash worths. Taxes will certainly be incurred on the gain, however, when you surrender the plan. You may borrow on the cash money worth of the policy, however bear in mind that you may sustain a substantial tax obligation expense when you give up, also if you have borrowed out all the cash value. The advantage is that improvements in rates of interest will certainly be mirrored faster in passion sensitive insurance than in traditional; the drawback, certainly, is that reduces in interest prices will additionally be really felt faster in rate of interest sensitive whole life. There are 4 standard passion sensitive whole life plans: The universal life policy is actually greater than passion delicate as it is made to reflect the insurance company's current mortality and expenditure as well as passion earnings instead than historical rates. The business credit scores your costs to the money value account. Regularly the business subtracts from the cash money value account its costs and the price of insurance defense, typically explained as the mortality deduction charge. The balance of the money value account collects at the passion attributed. The business assures a minimal passion price and an optimum death charge. These assurances are normally really traditional. Present assumptions are essential to interest delicate items such as Universal Life. When rate of interest are high, advantage projections(such as cash value)are additionally high. When rates of interest are reduced, these forecasts are not as appealing. Universal life is additionally one of the most flexible of all the various kinds of policies. The plan usually offers you an option to select one or 2 sorts of survivor benefit. Under one option your beneficiaries obtained just the face quantity of the plan, under the other they obtain both the face quantity and the money worth account. If you desire the optimum quantity of survivor benefit now, the second choice ought to be selected. It is necessary that these assumptions be sensible due to the fact that if they are not, you may have to pay more to keep the policy from lowering or lapsing. On the various other hand, if your experience is much better then the presumptions, than you may be able in the future to skip a premium, to pay less, or to have actually the strategy paid up at a very early date. On the various other hand, if you pay even more, and your presumptions are realistic, it is feasible to pay up the policy at an early date (the cost of 500 000 worth of 30-year term life insurance for fernando). If you surrender a global life plan you may get much less than the cash value account since of surrender costs which can be of 2 types.

You may be asked to make added costs settlements where protection might end because the rate of interest price dropped. The assured price supplied for in the policy is a lot lower (e.g., 4%).

What Is A Ten Year Term Life Insurance Policy

In either case you must get a certificate of insurance coverage explaining the provisions of the team plan and any insurance policy fee. Generally the optimum amount of insurance coverage is $220,000 for a mortgage and $55,000 for all various other debts. Credit history life insurance policy need not be acquired from the organization granting the loan

If life insurance policy is called for by a lender as a condition for making a financing, you might have the ability to appoint an existing life insurance policy, if you have one. You might wish to acquire team credit history life insurance in spite of its greater price due to the fact that of its ease and its availability, typically without thorough proof of insurability. what effect can a long-term care benefit rider have on a life insurance policy.

However, home collections are not made and premiums are mailed by you to the representative or to the business. There are certain variables that tend to increase the expenses of debit insurance coverage greater than routine life insurance policy plans: Specific costs coincide regardless of what the dimension of the plan, to make sure that smaller policies released as debit insurance coverage will have greater costs per $1,000 of insurance policy than larger dimension normal insurance coverage

Given that very early gaps are expensive to a business, the costs must be handed down to all debit policyholders. Because debit insurance coverage is created to include home collections, higher commissions and costs are paid on debit insurance coverage than on regular insurance coverage. Oftentimes these higher expenses are handed down to the policyholder.

Where a firm has different premiums for debit and normal insurance policy it might be feasible for you to purchase a larger amount of regular insurance policy than debit at no extra expense - extended term option life insurance. Consequently, if you are thinking about debit insurance, you need to certainly investigate normal life insurance policy as a cost-saving option.

Taxable Group Term Life Insurance

This plan is created for those who can not originally pay for the regular whole life premium yet that want the greater premium insurance coverage and feel they will at some point be able to pay the greater costs (renewable term life insurance advantages). The family members policy is a mix plan that offers insurance security under one contract to all participants of your prompt family members partner, partner and children

Joint Life and Survivor Insurance policy provides protection for 2 or more persons with the survivor benefit payable at the death of the last of the insureds. Costs are substantially lower under joint life and survivor insurance policy than for policies that guarantee just one person, because the chance of needing to pay a fatality case is lower.

Premiums are significantly higher than for policies that guarantee one person, considering that the chance of needing to pay a death case is higher (a return of premium life insurance policy is written as what type of term coverage). Endowment insurance policy attends to the repayment of the face total up to your beneficiary if fatality takes place within a particular time period such as twenty years, or, if at the end of the specific duration you are still to life, for the repayment of the face quantity to you

{kind=link}

Latest Posts

When Does A Term Life Insurance Policy Matures

$25,000 Term Life Insurance Policy

Decreasing Term Life Insurance Quotes